The Stock Exchange is a 200-Year-Old Tool Being Used to Solve a 2025 Problem

Nobody really talks about what we really lost when companies stopped going public early. The conversation always frames it as maturity, sophistication, the private markets just got better. And sure, that is technically true. But there is something worth pulling apart in that framing.

Microsoft went public in 1986 at a $778 million valuation. Bill Gates was 30 years old. The company had been around for eleven years but the public got in early enough that a $1,000 investment at IPO was worth over $400,000 twenty years later. Home Depot listed two years after it was founded, when it had only four stores. The people who bought in at that stage participated in the actual building of something. That was the implicit contract between public markets and ordinary investors. You take the early risk, you get the early upside. The system was not perfect but it was at least pointed in the right direction.

That contract got quietly torn up sometime in the last two decades and most people did not notice until the returns stopped showing up.

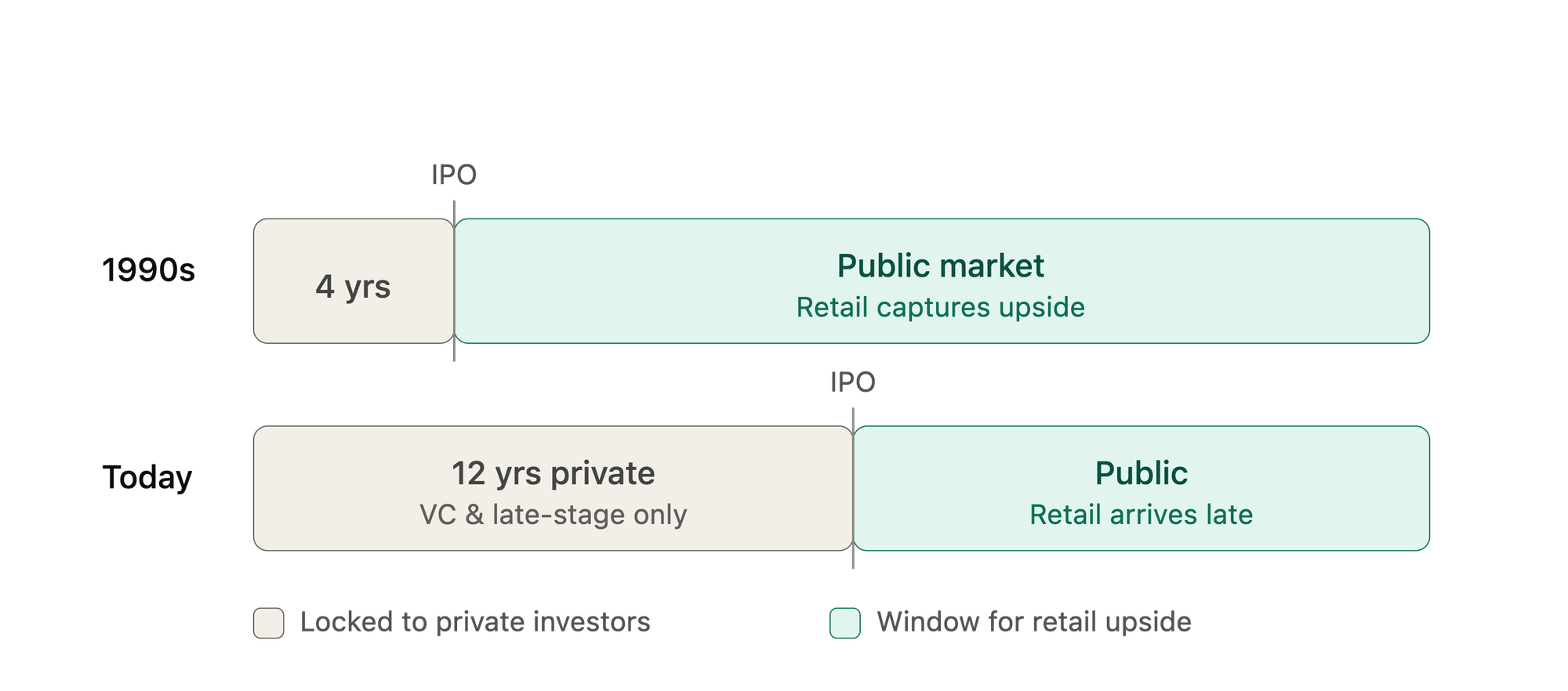

The average time from founding to IPO has gone from roughly four years in the 1990s to over twelve today. Uber spent a decade as a private company, raising at valuations that kept climbing, before anyone outside its cap table could buy a share. By the time it listed in 2019 it was already worth over $80 billion and the stock basically went nowhere for years afterward. The people who made real money on Uber were not public market investors. They were venture funds and late-stage private investors who got in during the years the public never saw, which is no coincidence. That is the system working exactly as it was redesigned to work, just not for you.

Airbnb is the same story. Founded in 2008, went public in 2020. Twelve years of private growth before retail investors could touch it. The IPO popped 113% on the first day which sounds exciting until you realize that pop was just the public market rapidly catching up to a valuation that private investors had been sitting on for years already. The excitement was real. The opportunity had already passed.

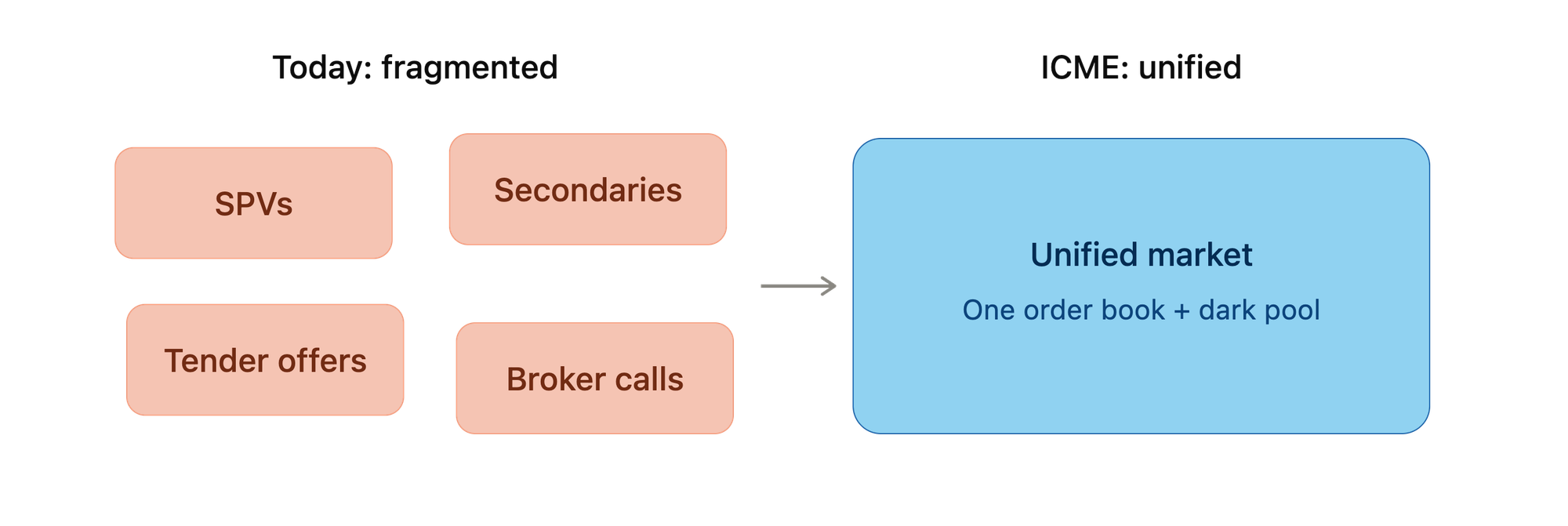

What filled the gap was a patchwork. SPVs, secondary platforms, tender offers, broker calls, side vehicles that do not show up cleanly on cap tables. Secondary SPV volume grew over 500% in two years, which is not a story about innovation but about people building complicated workarounds because the front door has been locked for decades. The workarounds keep multiplying, and almost without exception they require either a large minimum check or a warm introduction to someone who knows someone. The structural beneficiary of the current arrangement is not the retail investor. It never really was.

And that points to the real issue. Demand was never the problem. The infrastructure to meet it was. The secondary market for private shares is not some niche curiosity. It is a multi-billion dollar shadow ecosystem that exists entirely because public market infrastructure was never updated to serve this stage of a company's life. The exchange was built for a world where companies showed up after a decade of seasoning, with institutional sponsorship and analyst coverage already lined up. It has no real answer for a company that is seven years old and growing fast and has zero interest in spending thirty million dollars on an IPO process that will consume management bandwidth for the better part of a year. The infrastructure did not fail to evolve because the problem was hard to see. It failed to evolve because the people closest to it had little incentive to change it.

So the gap just sits there. A secondary broker who knows a seller. An SPV that closes before most people hear about it. A tender offer with a short window announced to a small list. If you are inside the network you navigate it. If you are not, you buy the company on a brokerage app five years later when the multiple has already done most of its work and wonder why it feels like you are always arriving late.

ICME is building directly into that gap and the design choices reflect a clear view of what the actual problem is. The target is not every startup. Not synthetic wrappers around companies that never agreed to be tokenized. The beachhead is recognizable growth-stage companies, typically somewhere in the Series B to early growth range, $100 million to $1 billion in valuation, with real product-market fit and a community that actually cares. And unlike most of what currently exists in this space, the actual issuer is behind it. That distinction matters because it changes the entire character of what comes after.

When the company itself is issuing tokenized common shares into a regulated primary offering, what gets created is not another workaround but something the current system has never offered. An official, continuous market around real equity, built specifically for this stage of a company's life. A Solana order book with visible bids, asks, depth, and a public reference price forming in real time rather than being negotiated over the phone. A Canton dark pool for institutions that need to move blocks without pushing the price against themselves. A bridge connecting both venues so liquidity stays unified instead of fragmenting into disconnected pools. KYC-linked wallets, on-chain audit trails, market surveillance. The compliance layer is architecture, not an afterthought. That is what makes the market trustworthy rather than just functional. It is also what separates a platform that serious issuers and serious investors can rely on from the synthetic workarounds that have filled the space so far.

The royalty mechanic is where the issuer psychology shifts. The company earns a royalty on secondary trading, seventy percent of transaction fees on qualifying trades going back to the issuer. Healthy trading volume stops being a cap table nuisance and starts being something the company has a genuine financial interest in supporting. Secondary liquidity becomes an asset rather than something the legal team quietly manages in the background. In the current private market setup, when shares trade informally the economics flow to intermediaries and the headache flows to the company. ICME inverts that relationship. A healthy secondary market around a company's equity can mean customers becoming owners, employees seeing real value in their equity, a live price signal forming before any IPO process begins, and royalty income generated without issuing a single new share. The company is not just tolerating a market around its stock. It is participating in one it actually has a reason to want.

The three things missing from private company equity have always been the same: a regulated path for real investors to get in early, a legitimate place to trade afterward, and an issuer that actually has a reason to want that market to be healthy. They have just never existed together in one place. Whether ICME closes that gap permanently is a question the market will answer. But the demand has been visible for years, and the workarounds that have filled the space in the meantime have made one thing clear: a market built specifically for this stage of a company's life is long overdue.